All Categories

Featured

Table of Contents

This plan design is for the consumer who requires life insurance policy however wish to have the ability to choose just how their money worth is spent. Variable plans are financed by National Life and dispersed by Equity Services, Inc., Registered Broker/Dealer Associate of National Life Insurance Policy Business, One National Life Drive, Montpelier, Vermont 05604.

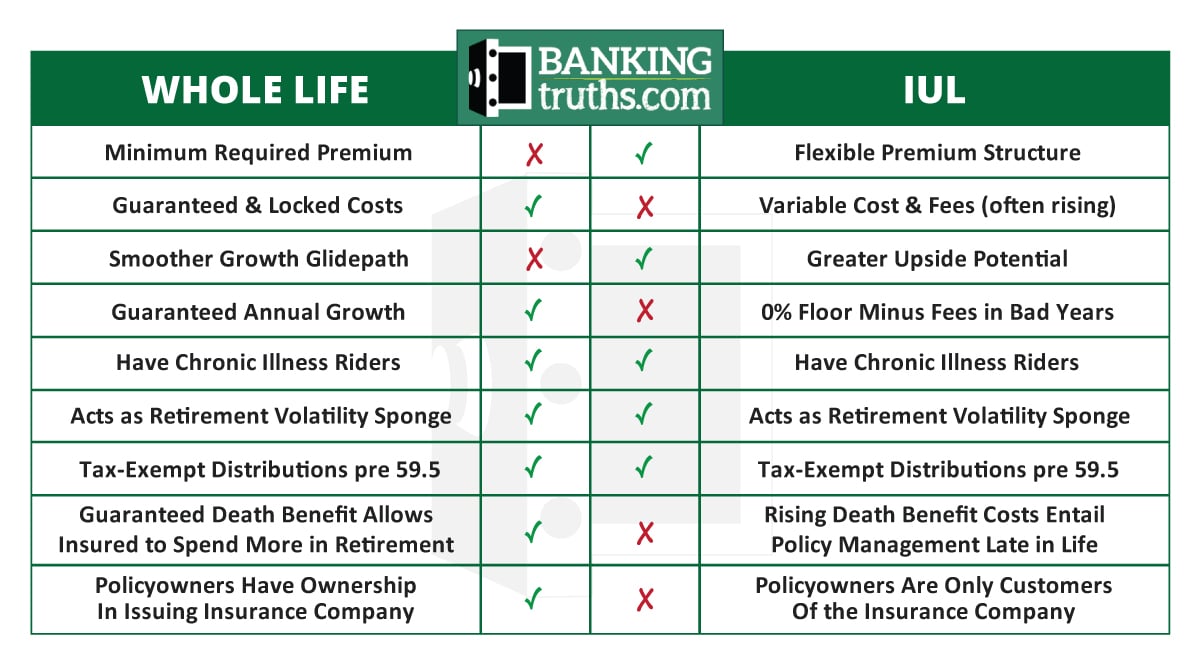

A whole life insurance policy policy covers you forever. It has cash money value that grows at a set rates of interest and is the most usual type of irreversible life insurance policy. Indexed universal life insurance policy is likewise long-term, however it's a details kind of global life insurance coverage with cash money value connected to a securities market index's performance as opposed to non-equity earned rates. The insurer will certainly pay out the face quantity straight to you and end your plan. Contrastingly, with IUL policies, your survivor benefit can enhance as your money worth grows, bring about a possibly greater payment for your recipients.

Learn more about the lots of advantages of indexed universal insurance and if this kind of policy is ideal for you in this useful article from Protective. Today, lots of people are looking at the value of long-term life insurance with its ability to provide long-term security together with cash money worth. Thus, indexed global life (IUL) has come to be a popular choice in supplying permanent life insurance policy protection, and an also greater potential for development via indexing of passion debts.

How do I choose the right Indexed Universal Life Account Value?

What makes IUL various is the way rate of interest is credited to your policy. In addition to using a traditional declared rate of interest price, IUL supplies the opportunity to gain passion, based on caps and floors, that is connected to the efficiency of a picked option of market indices such as the S&P 500, Dow Jones Industrial Standard or the Nasdaq-100.

With IUL, the insurance holder determines on the amount assigned among the indexed account and the taken care of account. Similar to a regular universal life insurance plan (UL), IUL enables for an adaptable premium. This indicates you can choose to add more to your policy (within government tax obligation law limitations) in order to assist you develop your cash money value also much faster.

As insurance policies with investment-like functions, IUL plans charge compensations and fees. These costs can decrease the cash money worth of the account. While IUL plans likewise use guaranteed minimal returns (which may be 0%), they likewise cap returns, also if your choose index overperforms (Indexed Universal Life account value). This indicates that there is a limit to price of cash worth development.

Written by Clifford PendellThe advantages and disadvantages of indexed global life insurance policy (IUL) can be hard to understand, specifically if you are not knowledgeable about just how life insurance functions. While IUL is one of the hottest products on the marketplace, it's likewise one of one of the most unpredictable. This sort of coverage could be a feasible option for some, however, for lots of people, there are better options avaiable.

What types of Guaranteed Iul are available?

If you have an adverse return, you will certainly not have an unfavorable crediting price. Instead, the price will usually be 0 or 1 percent. In addition, Investopedia listings tax obligation benefits in their benefits of IUL, as the survivor benefit (money paid to your recipients after you die) is tax-free. This is real, however we will include that it is also the instance in any type of life insurance policy policy, not just IUL.

The one point you require to understand regarding indexed global life insurance is that there is a market risk included. Investing with life insurance coverage is a various game than getting life insurance policy to shield your family, and one that's not for the faint of heart.

As an example, all UL items and any type of general account item that depends on the performance of insurance providers' bond profiles will certainly go through rate of interest risk."They proceed:"There are fundamental threats with leading customers to think they'll have high prices of return on this product. A customer may slack off on moneying the money worth, and if the plan doesn't do as expected, this might lead to a gap in insurance coverage.

In 2014, the State of New york city's insurance coverage regulator penetrated 134 insurance firms on just how they market such plans out of worry that they were exaggerating the possible gains to customers. After continued scrutiny, IUL was struck in 2015 with guidelines that the Wall Road Journal called, "A Dosage of Reality for a Hot-Selling Insurance Coverage Item." And in 2020, Forbes published and short article entitled, "Seeming the Alarm System on Indexed Universal Life Insurance Policy."In spite of numerous articles advising customers regarding these plans, IULs continue to be just one of the top-selling froms of life insurance policy in the United States.

What is the difference between Indexed Universal Life Interest Crediting and other options?

Can you take care of seeing the stock index choke up understanding that it directly affects your life insurance policy and your capability to safeguard your family members? This is the last gut check that hinders even incredibly rich investors from IUL. The entire point of getting life insurance policy is to lower danger, not create it.

Discover much more concerning term life here. If you are looking for a plan to last your entire life, have a look at assured universal life insurance policy (GUL). A GUL policy is not technically long-term life insurance policy, yet rather a hybrid between term life and universal life that can allow you to leave a legacy behind, tax-free.

Your cost of insurance policy will certainly not transform, also as you grow older or if your wellness changes. Your coverage isn't connected to an investment. You spend for the life insurance policy protection only, similar to term life insurance policy (IUL companies). You aren't pouring additional money right into your plan. Trust fund the economists on this: you're far better off putting your money right into a savings or perhaps paying down your home mortgage.

Why do I need Iul Loan Options?

Guaranteed global life insurance policy is a fraction of the expense of non-guaranteed global life. You do not run the risk of losing protection from undesirable financial investments or adjustments in the market. For an extensive comparison between non-guaranteed and assured global life insurance policy, click below. JRC Insurance Coverage Group is right here to help you find the ideal plan for your needs, without additional price or fee for our support.

We can retrieve quotes from over 63 top-rated service providers, permitting you to look past the big-box companies that usually overcharge. Consider us a buddy in the insurance coverage sector who will look out for your best passions.

What is Indexed Universal Life Policyholders?

He has aided hundreds of family members of services with their life insurance policy requires considering that 2012 and specializes with candidates who are less than best wellness. In his leisure he delights in spending time with family, traveling, and the open airs.

Indexed universal life insurance coverage can help cover many economic needs. It is just one of many kinds of life insurance coverage offered.

{kind=link}

Latest Posts

Index Assurance

Maximum Funded Tax Advantaged Life Insurance

Problems With Universal Life Insurance